How to Accept Credit Card Payments in Japan: Trends, Advantages, and Costs

Table of Contents

We help businesses accept payments online.

According to Japan’s Ministry of Economy, Trade and Industry, Japan’s cashless payment ratio in 2024 was 42.8%. Of those transactions, credit cards accounted for 83%, making them the most dominant cashless method in the country by far.

For foreign businesses operating or planning to enter Japan, offering credit card payments is essential for reaching modern consumers and ensuring smooth sales, both online and in-store. However, payments in Japan come with their own rules and customer expectations.

In this guide, we’ll walk through how credit card payments work in Japan, current usage trends, and what businesses should consider when selecting a payment service provider in Japan.

What Are Credit Card Payments in Japan?

Credit card payments are transactions in which a customer authorizes a business to charge their credit account for a purchase. The business is paid by a credit card provider, which collects funds from the customer later.

Japan’s credit card infrastructure encompasses domestic networks, such as the Japan Credit Bureau (JCB), as well as a combination of global and local compliance standards. These include PCI DSS, which governs secure handling of cardholder data worldwide. They also include Japan’s Installment Sales Act, which regulates how postpaid and installment-based payments are offered to consumers.

Unlike in the U.S., where consumers often carry balances and make minimum monthly payments, credit cards in Japan are generally expected to be paid in full by the next billing cycle.

Most Japanese cardholders use postpaid billing, with balances automatically deducted from their bank accounts at the end of the month. Installment and revolving options exist but are mainly used for large purchases and are less common. As a result, credit cards in Japan are viewed more as a convenient cash alternative than a borrowing tool.

Credit Card Usage Trends in the Japanese Market

Cultural attitudes toward credit cards have changed. Once seen as unnecessary or even risky, credit cards are now widely used for everyday purchases. Loyalty points, ease of recurring billing, and integration with mobile wallets have all contributed to this shift.

Major card issuers in Japan include:

- JCB (Japan Credit Bureau)

- Mitsui Sumitomo Card

- Rakuten Card

- Aeon Credit Service

- Sumitomo Mitsui Trust Club (Diners Club)

Usage Rate of Credit Cards is High in Japan

Credit cards are the most widely used cashless payment method in Japan, accounting for 83% of all cashless transactions in 2024, according to METI. Usage has grown steadily over the past decade, with the Japan Consumer Credit Association (JCA) reporting an annual transaction volume of over ¥73 trillion and an average of 2.8 credit cards per person.

For more information, see KOMOJU’s guide to payment methods in Japan.

Tap to Pay is Becoming More Widespread

While prepaid IC cards, such as Suica and Pasmo, once dominated mobile payments, credit-based Tap to Pay (contactless NFC payments) is becoming increasingly common.

As of 2025, Japan’s mobile payments market is valued at $173 billion, driven by rising smartphone adoption, e-commerce growth, and a significant shift toward contactless transactions—particularly in large cities such as Tokyo, Osaka, and Yokohama.

The Japan Mobile Payment Association projects that mobile payment transactions will exceed ¥12 trillion. Proximity payments, such as Tap to Pay, are expected to lead adoption because they are integrated into transport systems and retail checkouts.

Businesses entering the market should consider enabling this fast, mobile-friendly checkout experience. KOMOJU’s Tap to Pay integration allows merchants to accept NFC credit card payments through modern terminals and devices.

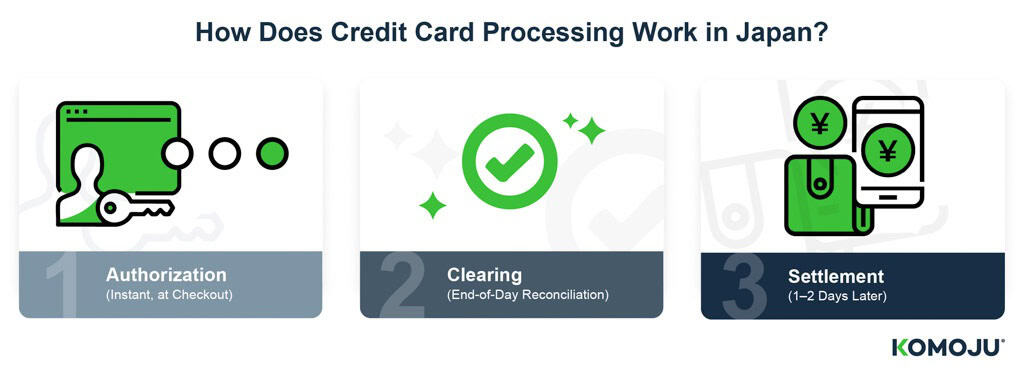

How Does Credit Card Processing Work in Japan?

Credit card payments in Japan adhere to a global standard structure, but with local caveats and preferences. There are three core phases: authorization, clearing, and settlement.

Step 1: Authorization (Instant, at Checkout)

- A customer presents a credit card at checkout—by inserting the chip, swiping, or using a mobile option like Apple Pay or PayPay.

- The business’s payment system (such as a terminal or online checkout) sends a request to their payment processor or bank that handles credit card payments.

- This request is routed through the card network (such as Visa, Mastercard, or JCB) to the customer’s credit card company or issuing bank.

- The credit card company checks if the customer has enough available balance and approves or declines the transaction.

- If approved, a temporary hold is placed on the customer’s account, and the approval is sent back through the same network to the business.

In Japan, cashiers typically ask how the customer would like to pay—whether in a single payment or installments. Even websites like Amazon will offer installment payments at checkout.

Step 2: Clearing (End-of-Day Reconciliation)

- At the end of the day, the business submits all approved payments in a batch to their payment processor.

- The processor forwards this data through the card network to each customer’s credit card company.

- The credit card company finalizes the charges, removing the temporary hold and officially adding the amount to the customer’s statement. Customers may still have the option to convert the charge into installments or a revolving payment plan.

Step 3: Settlement (1–2 Days Later)

- The card network calculates the totals for all parties involved and settles the payments.

- The customer’s credit card company sends the funds—minus transaction fees—to the business’s payment processor or bank.

- The business then receives the payout in their bank account, either with the fees already deducted or billed separately, depending on the provider.

For international payments or cards, foreign exchange conversion is handled at this stage.

How to Accept Credit Card Payments

To accept credit cards in Japan, businesses need tools that support both domestic card brands and local payment expectations.

Online Acceptance Methods

Credit card payments for online sales are typically processed through e-commerce platforms or links that direct the customer to a secure checkout.

E-commerce Payment Gateways

KOMOJU’s e-commerce integrations let you connect with platforms like Shopify and WooCommerce. These gateways handle credit card payments from both Japanese and international customers, including support for JCB and other major credit card brands.

Payment Links

Payment links are a simple way to request payment without a full website. You generate a secure link and send it by email or chat, allowing customers to pay by credit card with just a few clicks.

Offline Acceptance Methods

For in-person sales, credit card payments are processed through physical terminals or mobile devices that support tap or chip-based payments.

Payment Terminals

Payment terminals are used at counters or checkout areas. Modern payment terminals support chip cards, contactless cards, and mobile wallets. They are a standard option for larger operations, such as multiple stores and large restaurants.

Tap to Pay via Your Phone

With Tap to Pay, staff can accept credit card payments using a smartphone or tablet—no extra hardware needed. This setup is especially useful for pop-ups, delivery, and mobile sales.

Credit Card Integration: Payment Service Provider vs Direct

When integrating credit card payments, businesses typically choose between two approaches: working with a payment service provider (PSP) or building a direct integration with individual payment components (such as acquiring banks, gateways, and processors).

A PSP offers an all-in-one solution, handling processing, security, and settlement through a single contract and API or plugin. Direct integration requires working with each payment party separately, which offers more control but adds greater technical and operational complexity.

The table below outlines the key differences:

What to Consider | Using a Payment Service Provider (PSP) | Connecting Directly to Each Service |

How Long It Takes to Set Up | Fast to set up with ready-made tools, little coding needed | Slower setup, requires custom development and multiple vendors |

Security and Compliance | Provided by the PSP (like fraud protection and PCI requirements) | You’re responsible for protecting data and staying compliant |

Ongoing Management | Everything is in one place—easy to track and support | You’ll need to manage each provider separately |

Payment Options Available | Includes major cards, local brands (like JCB), wallets, and more | Limited unless you build in each option yourself |

Scaling Up | Easy to expand to new countries or add methods | Expansion requires more setup work and system changes |

Advantages of Credit Cards for Businesses

Cart abandonment is a major challenge in e-commerce. As of Q4 2024, 87% of online shopping carts in the Asia-Pacific region were abandoned before purchase (Statista, 2025). Reasons include trust, complexity, and a slow checkout.

According to Baymard Institute research, 18% of U.S. shoppers abandon their carts due to a “too long or complicated checkout process.” Offering fast and trusted payment options, such as credit cards, is one way to reduce friction.

It is equally important to build customer confidence in your site. Displaying security badges, recognizable card logos, and public reviews can significantly improve trust and completion rates.

Encourage Higher-Value and Impulse Purchases

Customers tend to spend more when using credit cards, especially for higher-priced items. According to Forbes Advisor, 58% of people say they spend more with a card than with cash, and they’re twice as likely to make an impulse purchase when paying by card. This behavior benefits merchants by increasing average transaction value.

In Japan, most credit card users pay their balance in full each month, but many cards offer the option to split payments into installments—either at checkout or later via the card issuer’s app or website. At physical stores, it’s common for cashiers to ask how many payments you’d like to make before completing the charge. This lowers perceived cost, making higher-priced items feel more affordable at the time of decision. It also makes payment in installments feel socially neutral, not like borrowing due to a lack of funds.

Simplify Sales Management

Fast, reliable checkout doesn’t just benefit the customer—it also simplifies day-to-day operations for the merchant. Accepting credit card payments through an integrated provider helps you:

- Track sales more accurately across channels.

- Reduce manual errors from cash handling or handwritten receipts.

- Sync payment records with bookkeeping tools or accounting software.

- Speed up reconciliation and reporting at the end of the day.

This clarity makes it easier to manage taxes, monitor performance, and stay organized, whether you’re running a small online store or a multi-location business.

Card payments also support smoother customer service. Staff don’t need to calculate change, and transactions are timestamped and traceable. This helps with refunds or dispute resolution.

Reduce Risk of Uncollected Payments

Unlike invoicing or bank transfers, card payments confirm the customer has sufficient credit, reducing the chance of bounced payments or lengthy collections.

Many cards also support recurring billing and retry logic, which helps prevent missed payments for subscription services or memberships.

With KOMOJU, merchants can accept secure payments upfront, minimize manual follow-ups, and maintain steady cash flow. This is especially important for high-volume or time-sensitive businesses.

Disadvantages of Credit Cards for Businesses

While credit cards offer convenience for customers, they do have drawbacks for merchants. The most common concerns include fees, failed payments, and exposure to fraud.

Transaction Fees Eat Into Margins

Accepting credit cards means paying transaction fees on every sale. Globally, average fees hover around 2.4% per transaction, according to ClearlyPayments, and rates of 1.9–3% are typical in Japan. While small, these costs directly reduce profit, especially for small businesses with tight margins.

Risk of Payment Failures

Not all card payments go through. Visa and Mastercard data indicate that ~15% of recurring card charges fail. However, one-time online transactions succeed 80–90% of the time—lower than the ~97% approval rate for in-person purchases. Each decline means a lost sale and potential customer frustration.

Exposure to Fraud and Chargebacks

Due to Japan’s aging population, credit card fraud is a serious risk—especially as payments switch to the digital realm. According to the Japan Credit Association (一般社団法人日本クレジット協会), credit card fraud losses in Q4 2024 amounted to ¥16.23 billion, representing a 22.3% increase compared to the previous quarter. .

Globally, fraud costs hit $48 billion in 2024, and for every $1 lost, merchants incur an average of $3.35 in total costs, including chargebacks and fees. “Friendly fraud” is a major issue. Over 70% of chargebacks now stem from customers falsely disputing charges, and merchants win only 45% of these cases.

Lengthy Payout Cycles

Credit card funds aren’t available immediately. Payouts typically take 1–3 business days, but some providers may delay payment for up to a week or more due to risk holds.

In Japan, delays are longer—acquirers may remit funds only once or twice a month, such as on the 15th or at the end of the month. This can create serious cash flow gaps for businesses that rely on steady liquidity.

Benefits of Credit Cards for Customers

Credit cards remain a preferred payment method for many shoppers in Japan and abroad—not just for convenience, but for the added value they bring.

Credit Card Rewards

One of the biggest incentives for using credit cards is the ability to earn points on every purchase. In Japan, nearly all major card issuers offer a points system (ポイント還元, pointo kangen), where users receive a set percentage of their spending back in the form of redeemable points.

- For example, a card may offer 1–2% back in points. Spend ¥10,000 and earn 100–200 points.

- Points can often be exchanged for digital gift cards, travel rewards, or cash back.

- Many cards also boost point earnings at specific merchants (e.g., Rakuten Card for Rakuten users).

These rewards accumulate automatically. They are often easy to redeem through an app or online portal, so many consumers choose credit cards that give the best return on their spending.

Seamless Payments

Credit cards offer a smooth and fast checkout experience—especially important for mobile shopping and digital wallets. Shoppers can skip entering bank details and avoid the extra steps required with cash or convenience store payments.

- For in-store purchases, tap-to-pay (contactless) is now widespread.

- Online, credit cards often integrate with autofill, Apple Pay, Google Pay, and other apps.

- Many Japanese shoppers also appreciate the option to split payments (分割払い, bunkatsubarai), which can be selected directly at checkout.

Costs of Credit Card Payments

Accepting credit card payments involves several types of fees, including both one-time and ongoing costs. These can vary based on provider and country. The table below applies to the Japanese market.

Cost Type | Description | Typical Range | Notes |

Initial Setup Fee | One-time cost for setting up a merchant account or payment terminal. | ¥0 – ¥50,000+ | Many online payment providers waive this fee; however, hardware terminals may incur additional costs. |

Monthly/Service Fee | Recurring fee charged for account maintenance or access to the processing platform. | ¥1,000 – ¥5,000 per month | May include access to dashboards, reporting, and support services. |

Transaction Fee | Fixed fee per transaction. | ¥10 – ¥30 per transaction | Usually combined with a percentage-based processing fee. |

Processing Fee | Percentage of each transaction value. | 1.5% – 3.5% (Japan avg. ~1.9%) | Varies by card type (Visa, Mastercard, Amex) and provider. |

Chargeback Fee | A fee is charged when a customer disputes a transaction. | ¥1,000 – ¥3,000 per case | Costs increase when chargebacks are frequent. |

Payout Delay Impact | Indirect cost due to delayed access to funds | 1–7+ day lag (Japan often 2x/month payout) | It can affect cash flow planning for smaller businesses. |

Payout Cycle

Unlike cash or instant transfer methods, credit card payments are settled in batches and paid out after a delay. For most businesses in Japan, payout cycles typically range from 2 to 7 business days, although some acquirers settle only once or twice a month. These delays can impact cash flow, especially for businesses with tight operating margins.

KOMOJU offers more flexibility than many traditional payment gateways. Merchants and platform operators can choose between two payout cycle options:

- Weekly payouts

Funds are transferred every Friday for transactions captured between the previous Saturday and Friday. - Monthly payouts

Funds are transferred at the end of the month for transactions from the previous month.

You can also set a minimum settlement amount to avoid small transfers. For example, if the threshold is set to ¥100,000 and the balance is only ¥50,000 by the cutoff, the payout will be deferred until the next cycle.

This flexibility helps businesses manage their cash flow more effectively by avoiding small, frequent payouts that could lead to extra fees.

Major Credit Card Brands in Japan

Below are popular and major credit cards offered in Japan.

- Visa (ビザ): The most widely accepted card brand in Japan and abroad. Visa cards are issued by most banks in Japan. Learn more about Visa in Japan

- Mastercard (マスターカード): Similar in reach to Visa, Mastercard is accepted almost everywhere in Japan. Learn more about Mastercard in Japan

- JCB (ジェーシービー): Japan’s leading domestic card brand, often preferred by local consumers. Learn more about JCB in Japan

- American Express (アメリカン エキスプレス): Popular among business travelers and affluent customers. Learn more about American Express in Japan

- Rakuten Card (楽天カード): Issued by Rakuten Group, this card is one of the most popular in Japan, especially among online shoppers. Cardholders earn Rakuten Points, which can be used across the Rakuten ecosystem.

How to Choose a Payment Service Provider

Selecting the right PSP directly impacts how smoothly your customers can pay, how quickly you receive funds, and how much you spend on fees.

Supported Payment Methods

Your PSP must support the payment methods your customers actually use. In Japan, this includes credit cards, convenience store payments, and digital wallets like PayPay and Rakuten Pay. Customers are more likely to abandon checkout if their preferred method isn’t available.

Payment Fees and Costs

Look for transparent pricing. Some PSPs charge setup fees, monthly fees, or hidden administrative costs, which can be difficult for small or seasonal businesses to absorb.

KOMOJU has no sign-up or monthly fees—businesses only pay per transaction.

Payout Cycle

Consider how quickly you receive your funds after a customer makes a payment. Some providers offer daily or weekly payouts, while others operate on slower monthly schedules.

Delayed payouts can create cash flow issues, particularly for businesses with high inventory or fast sales turnover.

KOMOJU offers flexible payout cycles—weekly or monthly—so businesses can choose the option that best aligns with their operations.

Fraud Detection System

Online payments come with fraud risk. Without strong prevention tools, businesses face chargebacks or damage to their reputation. Once a customer loses your trust, they’re unlikely to return.

KOMOJU offers free AI-driven fraud detection, enabling the identification and blocking of suspicious activity in real-time.

Ease of PSP Implementation

Integration should be fast and reliable. A PSP that supports common e-commerce platforms or offers well-documented APIs helps reduce development time and errors.

KOMOJU supports integration with major e-commerce platforms and offers full API documentation for custom setups.

Multi-Channel Support

If you sell both online and offline, it’s more efficient to use a single PSP that can handle all channels.

Multi-channel support enables easier sales tracking, report management, and a unified customer experience.

Summary: Credit Card Payments Are Essential for Business in Japan

Credit cards are a core payment method in Japan, widely used both online and in physical stores. Shoppers expect fast, familiar, and secure checkout experiences—and card payments deliver on all three. They also support flexible spending, reward programs, and installment options that appeal to a broad range of customers.

For merchants, credit cards can improve sales and expand reach, but they come with operational and cost considerations. Choosing the right partner makes all the difference.

KOMOJU supports businesses with simple, reliable credit card payment solutions:

- Payment links for simple checkout, no e-commerce site required

- Online store integration via major e-commerce platforms and APIs

- Tap to Pay transforms your smartphone into a contactless payment device

- Terminal solutions for in-person retail checkout

KOMOJU is built for Japan’s payment preferences—so you can focus on your customers, not your payment backend.

We help businesses accept payments online.