We help businesses accept payments online.

Despite being the fourth-largest e-commerce market in the world, Japan remains largely untapped by non-Japanese brands.

A big part of that is because there’s a prevailing idea that Japanese consumers only want to buy from Japanese brands.

In reality, that’s not the case at all. LL Bean is booming here. Zara is big here. IKEA — after an initial wobble — is popular here. So are KitKat, Braun, Cybex, and many more.

In fact, Japanese consumers actively seek out international brands when they can’t find the same product, or the same quality, domestically.

They’re also drawn to foreign products that feel authentic to their origins — LL Bean’s outdoor gear, for example — or from regions with a strong reputation in specific categories. Children’s products that meet European child safety standards are really popular here, too. And like shoppers everywhere, they’ll buy from overseas when the value is right.

So why don't more overseas brands sell here?

The fact that more global brands don’t sell in Japan is rarely about demand.

Most of the time, overseas brands underperform in Japan because of a handful of operational nuances that tripped them up post-launch.

Things like a checkout that doesn’t support the payment methods Japanese shoppers use day-in-day-out. Or a store that wasn’t built for mobile. Or product listings that don’t meet the detail Japanese consumers expect before they’ll buy.

So this guide covers what you need to know before entering Japan’s eCommerce market. We’ll explore how the market works, how Japanese consumers shop and what they expect, which platforms to sell on, how to localize effectively, and, most importantly, how to get payments right so you can find the best way to enter Japan’s eCommerce market.

What the Japanese eCommerce market means for cross border eCommerce merchants

Before we dig into the specifics of selling in Japan, let’s look at the numbers.

Japan’s B2C eCommerce market reached approximately $175 billion (¥26.1 trillion) in 2024, up 5.1% year-on-year.

In fact, it’s grown every year for a decade with compound annual growth rate (CAGR) sitting at around 7% and nothing to suggest that market size is going to change anytime soon.

But where it gets really interesting is when you look at overseas brands.

A lot of headlines are dominated by a study that found that 95% of eCommerce sales in Japan are domestic, which has led to the idea that Japanese consumers strongly prefer shopping from Japanese-operated stores.

And while that statistic is true, the conclusion isn’t quite as simple.

In 2023 alone, Japanese consumers spent approximately $21 billion (¥3.1 trillion) on US-based sites, up 6% year-on-year. That number has been climbing consistently since.

Fast forward to late 2025, and Rakuten announced that over 1,000 international merchants are now selling to Japanese consumers, and their sales are growing at double-digit rates.

And a huge independent study across 50+ payment methods found that just offering konbini payments to Japanese customers saw a 27% increase in conversion.

That’s not a sign that Japanese customers don’t buy from overseas. But it is a very clear indication that you need to adapt how you sell for the Japanese customer.

In other words, it’s not as simple as adding yen as a currency in your Shopify dashboard and watching the Japanese sales roll in.

The first thing to know about driving sales in Japan is how Japanese customers actually shop

Picture a customer in Texas or London or Sydney who can’t find their preferred payment method on your checkout. Statistically, 80% of the time, they’ll find another payment method and check out anyway.

The same thing doesn’t happen in Japan.

In fact, over 60% of Japanese shoppers abandon their cart entirely if their preferred payment method isn’t available. Japanese customers don’t want to adapt to your checkout, they expect your checkout to adapt to them.

We’re going to really explore the nuances of payment methods properly a little later on because it’s the biggest difference maker, but even that little detail alone tells you almost everything you need to know about selling here.

Japanese eCommerce isn’t just a different territory, it’s a different set of expectations. And winning in Japan means adapting to different rules on how payment works, how trust is built, how loyalty is earned.

Trust is everything in Japan, but especially for online stores

Japanese consumers are famously cautious shoppers. They research products thoroughly, read customer reviews carefully, and place significant weight on brand reputation before buying.

But the good news is that shoppers who do buy tend to be loyal and have high lifetime value.

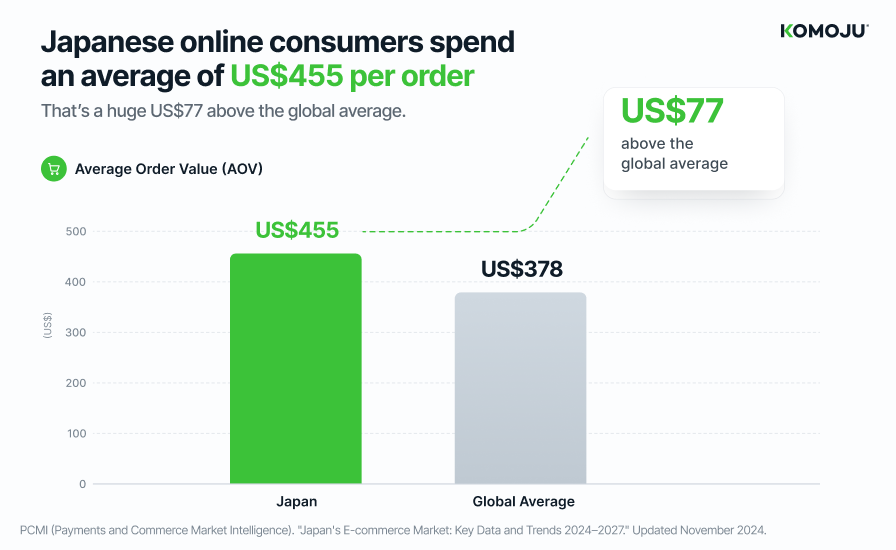

In fact, Japanese online consumers spend an average of US$455 per order, which is a huge US$77 above the global average.

By offering Japanese customers the payment methods they expect to see at checkout, you can remove obstacles from the checkout process, reduce abandoned carts and build brand loyalty all at the same time.

Mobile commerce is important, but desktop experience matters too

In 2024, mobile commerce accounted for approximately 65% of total eCommerce transactions in Japan, driven by mobile-optimized platforms, digital wallets, and streamlined checkout experiences. Like anywhere around the world, your store needs to work on mobile first.

However, Japanese consumers also tend to research heavily on mobile before completing purchases on desktop, meaning a poor experience on either device will cost you at a different stage of the same journey.

That means that your pages need to load fast, product information needs to be accessible without zooming or scrolling past walls of text, and checkout needs to be frictionless on a small screen.

Loyalty programs aren't just for retention in Japan

In most markets around the world, loyalty programmes are primarily a retention tool. They’re a way to keep customers who already like you coming back.

But in Japan, they’re also a discovery tool.

Almost half of Japanese consumers choose where to shop based on the presence of a rewards system, before they’ve decided on a product.

In fact, Rakuten Points alone is used by nearly 60% of Japanese consumers, and it’s integrated across Rakuten’s marketplace, credit card, travel, and banking services. Which means a shopper might choose your product over a competitor’s not because of your product, but simply because buying it through Rakuten fits into their points strategy.

Japanese consumers buy from stores built for them

There’s a statistic that you might have seen that says that only 10% of Japanese consumers buy from overseas websites, compared to 54% of Americans.

And it’s easy to look at that and think that means you shouldn’t launch in Japan.

But that’s not the case.

The difference is that lots of brands launching into Japan do a quick translation of their content, add yen to their checkout and run some ads.

And Japanese consumers are sensitive to signals that a store wasn’t built for them. Like we already discussed, trust in Japan is paramount.

So if they see prices in dollars or no konbini payments at checkout or shipping terms buried in small print or a returns policy that doesn’t exist, those things read the same way: this brand doesn’t understand us.

But a store that gets those things right — local currency, local payment methods, clear shipping, detailed product information — is set up to convert Japanese customers, even without brand recognition.

The big one: offering Japanese payment methods is non-negotiable

This is where most foreign merchants underestimate Japan.

We said it before, but it bears repeating: Japanese consumers have deeply established payment habits and when their preferred method isn’t available at checkout, over 60% will abandon their cart entirely rather than adapt.

Credit cards are still the most widely used payment method, but Japan’s checkout landscape is far broader than that.

Konbini payments — where you order online and then pay in cash at any of Japan’s 56,000+ convenience stores — are used by over 20% of online shoppers.

PayPay, Japan’s dominant QR code wallet, has over 70 million registered users, that’s nearly 50% of everyone in Japan.

Rakuten Pay is woven into the loyalty ecosystem that drives repeat purchases across the country.

Bank transfers are the default for high-value purchases among shoppers who won’t put card details online.

That’s one of the reasons that marketplaces like Amazon or Rakuten or TikTok Shop are doing well here right now, because these payment methods are being automatically handled and offered by the platform.

That’s why KOMOJU connects your store to all of Japan’s major payment methods — konbini payments, PayPay, Rakuten Pay, bank transfer, carrier billing – all through a single integration, with no Japanese legal entity required.

Why a lot of brands use Japanese marketplaces like Amazon Japan or Rakuten for market entry

We know that a lot of foreign merchants launching in Japan start on Amazon Japan or Rakuten Ichiba, and there are good reasons for that:

- You don’t need a Japanese legal entity to sell on either

- The payment infrastructure is already built in. Japanese shoppers can pay for your products however with their preferred payment methods with no friction

And that’s a great way to test Japan and prove demand.

But there are trade-offs.

On Amazon, you’re competing on price and fulfillment speed with fees that run at 8–15%. You also don’t control the customer relationship, the data, or the ability to run your own funnels and ads.

And while Rakuten gives you more brand control and access to its loyalty ecosystem, onboarding is demanding for an international seller. Japanese-language listings and customer service are non-negotiable, the merchant server runs entirely in Japanese, and setup fees run around $400 (¥60,000) upfront plus monthly costs of $130–$670 (¥19,500–¥100,000).

Again, that makes sense short-term, but that old idiom holds true here: you’re borrowing an audience on both platforms, not building one.

The goal for most brands launching in Japan is eventually a direct store.

But there are two things that tend to stop most brands from launching their own store in Japan: local entity requirements and payments.

What is a local entity? And why does it matter?

In most markets, a foreign brand can start selling online without any formal local presence.

You set up your store, point a payment gateway at it, start taking orders.

Japan works a little differently, but it’s not because of a single government rule that says you must incorporate locally, but because of how Japanese payment networks operate.

Each of Japan’s major payment methods — think konbini networks, PayPay, Rakuten Pay, bank transfers — is run by a separate provider, each with its own merchant agreement process.

And those agreements typically require the merchant to either be a Japanese-incorporated entity or work through a registered local intermediary.

Without that local entity, you can’t access the payment methods directly. You can sell into Japan, but you can’t give Japanese shoppers the checkout they expect.

This is why the marketplaces feel like the only option for so many brands. Amazon and Rakuten have already done this work and you piggyback off of it. Their payment infrastructure covers everything you need.

Which is why KOMOJU works exactly the same way

KOMOJU is a registered payment service provider in Japan with existing relationships across every major payment network.

When you integrate KOMOJU, you’re not just adding a payment gateway, you’re inheriting an out-of-the-box set of merchant agreements that would otherwise require a Japanese entity and months of individual negotiations to replicate.

No local entity required. No separate contracts. One integration.

And, as you’ll see in a minute, adding Japanese payment methods that cater to all consumer preferences is vital if you want to sell in Japan.

How shopping in Japan is influenced by its unique payment culture

There are lots of articles on the internet that look at all the different payment methods for selling into Japan. Which means you probably already know that you need konbini payments or PayPay or Rakuten to grow in Japan.

But to really understand why it makes a difference, it’s important to understand Japanese payment culture.

Japanese society’s relationship with money is unlike most Western markets, and that relationship makes a huge difference to payment behavior at checkout. Because while Western consumers might prefer certain methods, in Japan it goes much deeper than just “I prefer to use konbini payments”.

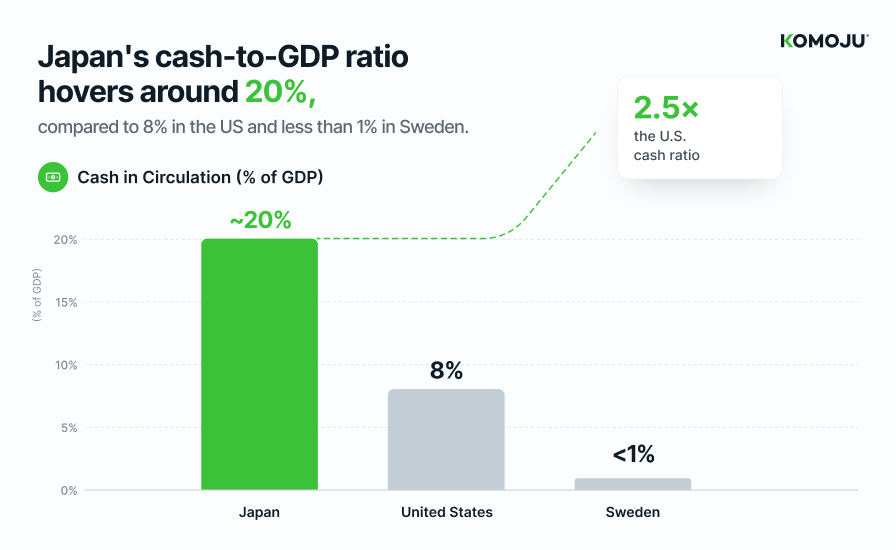

For starters, Japan’s cash-to-GDP ratio hovers around 20%, compared to 8% in the US and less than 1% in Sweden. There’s even a Japanese term for money kept at home rather than in a bank: tansu yokin, or literally “savings in the chest of drawers.”

In fact, estimates suggest around 50% of Japan’s currency in circulation isn’t actually circulating, it’s sitting in people’s homes. This is a reflection of a long-standing cultural relationship with cash that sees it as something tangible, safe, and entirely within personal control.

Another nuance is Japan’s relationship with debt. Japan’s credit card penetration is around 70% — which is slightly higher than the US — but average credit card debt is significantly lower because Japanese cardholders rarely use revolving credit.

Credit cards are adopted across Japan, but they’re just used carefully, and often paid off in full. That’s because, in Japan, debt carries a cultural weight that has no real Western equivalent. It’s traditionally tied to shame in a way that shapes how people think about using their credit cards.

On top of that, there’s a specific anxiety around entering card details online.

In 2024, credit card fraud losses in Japan hit a record ¥55.5 billion (approximately $370 million) per the Japan Consumer Credit Association. On top of that, 93% of that fraud occurred through identity theft at eCommerce businesses.

For a Japanese consumer visiting an unfamiliar foreign-language store for the first time, card anxiety is top of mind.

Why having Japan's alternative payment methods on your checkout is so important

For example, konbini payment isn’t a workaround for people without cards, it’s a conscious choice by people who have cards but prefer the security of cash.

PayPay and other digital wallets let people spend digitally without the psychological exposure of credit. Bank transfers for high-value purchases make intuitive sense when you understand that entering card details online feels like a specific, documented risk rather than a routine transaction.

And as we’ve already mentioned, a 2022 survey by JACCS Payment Solutions found that over 60% of Japanese shoppers abandon their cart entirely if their preferred payment method isn’t available.

The payment methods your checkout supports aren’t just about convenience features in Japan like having Apple Pay or Klarna is around the world.

For Japanese customers, having these payment methods acts as a signal about how secure, trustworthy and catered-to-Japan your store is.

How to add Japanese payment methods to eCommerce platforms

Now, Japan’s payment landscape has fragmented into dozens of competing methods — digital wallets, IC cards, carrier billing, bank transfer networks, konbini systems — each with its own user base, its own merchant agreements, its own technical integration.

You don’t need all of them in your store. But you need enough of them that your Japanese customers can pay the way they prefer.

Konbini payments are about letting customers buy something online and then go and pay for it in cash at their local konbini. (Think 7-11 or convenience store.)

And these payments exist because cash is trusted in Japan in a way that has no Western equivalent.

At your checkout, the shopper selects konbini payments and receives a reference code. They take it to any convenience store — 7-Eleven, Lawson, FamilyMart — pay cash over the counter, and confirmation arrives within the hour. You don’t ship until confirmed. (Which also eliminates chargebacks entirely.)

Over 20% of Japanese online shoppers use or plan to use this method. It’s not a fallback for people without cards, but as a deliberate preference by people who have cards and choose not to use them online.

With 56,000+ convenience stores nationwide and nearly half of Japanese consumers visiting one at least once a week, the infrastructure is already woven into daily life.

PayPay exists to give the next generation of Japanese consumers the convenience of digital payments without the psychological and cultural weight of credit.

With PayPay, you load it like a wallet and spend the money. That’s it.

There’s no debt. And it doesn’t require entering card details on a website. For a younger Japanese shopper, not seeing it at checkout is roughly equivalent to not accepting cards.

In fact, PayPay had over 70 million registered users as of July 2025, which is more than one in two people in Japan, rising to 72 million by December 2025. In fact, PayPay accounts for roughly 20% of all cashless transactions in the country, including credit cards.

When a customer uses PayPay at your checkout, all they need to do is select PayPay, scan a QR code with their app and make the payment. It appears instantly in your dashboard.

Rakuten Pay

Rakuten Points is used by nearly 60% of Japanese consumers and is integrated across more than 70 Rakuten services from shopping to travel to banking to mobile to beauty.

In fact, over 70% of consumers in Japan factor in point accumulation when deciding where to shop. Like we said before, in Japan, points aren’t a reward for spending. They’re a second kind of currency that customers use to decide where customers shop in the first place.

A Rakuten-loyal customer arrives at your checkout with accumulated points ready to use and a habit of shopping wherever those points work. Supporting Rakuten Pay isn’t just adding a wallet, it’s joining an economy that runs alongside the yen for tens of millions of people.

And as we noted earlier, you don’t need to sell on Rakuten Ichiba to participate in it. Accepting Rakuten Pay on your own store is enough, which is why it’s one of the payment methods supported by a KOMOJU integration.

Offering JCB in Japan is like offering Visa or Mastercard in western markets.

JCB is Japan’s only domestically-founded credit card brand. Founded in Tokyo in 1961, JCB was built specifically to serve Japanese consumers on Japanese terms. Over six decades it’s become embedded in the banking and loyalty infrastructure in a way that Visa and Mastercard simply aren’t with 169.8 million cardholders globally.

Many Japanese consumers hold a JCB card as their primary card, often through a co-branded product tied to their bank, their employer, or their loyalty programme. In fact, over 25% of Japanese eCommerce transactions are paid with JCB.

Pro tip: JCB acceptance isn’t automatic for foreign merchants. It has to be explicitly enabled through your payment provider. Without it, a customer who enters their JCB card at checkout sees a decline with no explanation.

Pay-easy is Japan’s online bank transfer system, integrated directly with the country’s major banks and ATM networks.

At checkout, the shopper receives payment details and completes the transfer through their online banking or at an ATM, with no card details entered. And because 98% of Japan’s population holds a bank account, Pay-easy makes your store accessible to virtually every Japanese consumer.

For significant purchases — electronics, luxury goods, anything where the order value creates hesitation about card exposure — some Japanese consumers actively prefer this method.

And given that 93% of Japan’s credit card fraud in 2023 occurred through identity theft at ecommerce businesses, account-to-account transfer isn’t overcaution. It’s a rational response to a documented and widely-reported risk.

Carrier billing

In Western markets, mobile carriers let you make calls and that’s pretty much it.

In Japan, the three major carriers — NTT Docomo, au by KDDI, and SoftBank — have spent decades positioning themselves as something closer to financial infrastructure.

NTT Docomo alone has over 80 million subscribers and has recently moved to acquire a major bank, integrating loans, mortgages, and savings directly into its mobile ecosystem. Docomo runs its own points programme — d Point — that earns and redeems across purchases and the phone bill itself. au and SoftBank have built similar ecosystems.

For a significant portion of Japanese consumers, their mobile carrier is already part of how they manage money, not just how they make calls.

Carrier billing lets your customers charge the purchase charges directly to the phone bill. And for younger consumers who may not yet hold a credit card, or digital product buyers who want the most frictionless path from intent to purchase, it removes every remaining barrier.

Worth noting: expectations around logistics and shipping are different too

Japan’s logistics infrastructure is world-class, which means customers have very high expectations around delivery. Same-day or next-day delivery is standard in Tokyo and other major cities, and most Japanese consumers expect precise and accurate delivery windows.

For merchants shipping from overseas, this might seem like a problem, but the solution is just to set clear and honest expectations. Japanese consumers are understanding about international shipping times when they’re communicated upfront, but they’re far less forgiving when deliveries are late without explanation.

If your Japan sales volume justifies it, it’s worth considering partnering with a local fulfillment provider or using Amazon FBA in Japan, which stores your inventory inside the country (much like a 3PL) and makes delivery so much faster for the consumer.

Getting started: adding Japanese payment methods to your store

At first glance, adding all of these different payment methods to your checkout can look like a lot of operational and logistical heavy lifting.

After all, each of Japan’s major payment methods is run by a separate company. That means separate merchant agreements, separate technical integrations, separate onboarding processes, all conducted in Japanese.

Konbini payments span multiple convenience store networks with their own backend systems. PayPay is one company. Rakuten Pay is another. au PAY is KDDI. Carrier billing means separate agreements with NTT Docomo, au, and SoftBank.

For a foreign merchant approaching this directly, you’re looking at months of negotiations (often in Japanese) before a single Japanese shopper can pay you in the way they prefer.

That’s exactly why we built KOMOJU.

We are a registered payment service provider in Japan with existing merchant agreements across every major payment network.

When you integrate KOMOJU, you’re not installing a payment gateway, you’re inheriting a set of relationships that took years to build and would take a foreign merchant months of Japanese-language negotiations to replicate.

One integration. No Japanese legal entity required. Over 60 payment methods across Japan, South Korea, China, Southeast Asia, Europe, and Brazil.

If you use eCommerce platforms — Shopify, WooCommerce, Wix, Magento, Salesforce Commerce Cloud — there’s a no-code plugin that lets you get set up fast.

For custom-built stores, we’ve got a full API with hosted pages, hosted fields, and a mobile SDK.

And for merchants who take payments outside a website or sell in person, payment links let you create a checkout page and send it directly to customers and KOMOJU Terminal and Tap to Pay feed everything into the same dashboard.

Here's how getting started with KOMOJU works:

You can get set up in just a few steps. Most merchants go live within a few days.

- Create your KOMOJU account. The application is online and takes a few minutes. You’ll need the same business verification documents you’d provide to any payment provider, but nothing Japan-specific. We will do a quick check on your product category and order details as part of the process for compliance, but for most merchants selling physical goods, it’s all straightforward.

- Connect your store. Whether you use Shopify, WooCommerce, Wix, Magento, Salesforce Commerce Cloud, sell offline or use a custom integration, KOMOJU is built to work around you. (For a full list of ways to integrate, visit our Integrations page.)

- Choose your Japanese payment methods. Toggle the payment methods you want to offer on-or-off and you’re good to go. All your Japanese payment methods will appear at your checkout automatically once connected and approved.

Full technical documentation at the KOMOJU getting started guide →

The bottom line: Japan is complicated, but it's worth it.

Japan looks complicated from the outside.

The language, the localization standards, the loyalty ecosystems, the payment infrastructure, the cultural expectations around trust and detail… it is a little more complex than adding a new currency and running ads.

However, most of the complexity is front-loaded.

Once you’ve found a way to adapt to Japan, it stops being complicated and starts being one of the most rewarding markets in the world.

High average order values. Genuinely loyal customers. Return rates a fraction of what you’d see at home. A consumer base that, once it trusts you, comes back again and again.

That’s exactly what KOMOJU is for.

We’re not just a payment gateway that supports Japanese payment methods, we’re a local infrastructure layer that took years to build — from the merchant agreements to the payment network relationships to the local entities and technical integrations — so that you don’t have to.

All you need to do is plug in, add it to your checkout and you can offer Japanese customers the freedom to choose the payment methods they need to see to feel comfortable checking out.

Case in point: how Steam grew in Japan with KOMOJU

In 2014, Steam was the world’s largest PC gaming platform and was growing fast everywhere. Except Japan.

But Japanese gamers wanted to spend money on PC gaming. It’s just that the Steam experience had been built for a Western audience and there were too many barriers for Japanese customers.

The interface was in English. Prices were in USD. The only payment option was an international credit card, which many Japanese consumers don’t use, and which others didn’t feel comfortable entering on a foreign-language site.

Customer support operated in English with a significant time zone gap.

In other words, everything was set up to send the signal that this wasn’t built for Japanese customers.

KOMOJU had been working with Valve since 2012, when they launched RPG Maker on Steam. The software became an unexpected global bestseller, and it revealed that Steam had enormous untapped potential in Japan if the platform could actually serve Japanese users.

So KOMOJU worked with Steam to localize their whole marketplace to Japan.

We helped them add Japanese-language support, yen pricing, konbini and other Japanese local payment methods so that they had a checkout that felt like any other local online purchase.

And in 2016, the year after the new checkout went live, Japan recorded the fastest growth in Steam users anywhere in the world.

That’s the power of a checkout that is built for Japanese customers.

Learn how KOMOJU helps international merchants accept Japanese payment methods

Selling in Japan: a quick summary and reference guide

| Must-have feature | Why it matters | How KOMOJU helps |

|---|---|---|

| Japanese language copy & content | Japanese consumers hold written communication to an exceptionally high standard. A poor translation reads as untrustworthy, which in Japan is often enough to damage trust in your brand. | KOMOJU’s hosted checkout pages display in Japanese natively, with payment confirmation emails sent to customers in Japanese too. That way, your payment experience feels local even if the rest of your store is still being localised. |

| Yen pricing | Japanese consumers are meticulous researchers who want certainty before they buy. Displaying prices in USD or euros introduces an uncertainty that runs counter to how Japanese shoppers make decisions. | KOMOJU processes all transactions in Japanese yen natively. |

| Great mobile and desktop experiences | Around 65% of Japanese eCommerce transactions happen on smartphones. However, older Japanese consumers — a significant and high-spending demographic — often prefer desktop for the final purchase. A great experience on both is crucial to fully capitalise on the market. | KOMOJU’s checkout is fully responsive across mobile and desktop. |

| Localized payment methods | In Japan, how you pay is a reflection of your relationship with money, trust, and security — not just convenience. Over 60% of Japanese shoppers abandon their cart if their preferred method isn’t available. | KOMOJU connects your store to every major Japanese payment method — konbini, PayPay, Rakuten Pay, au PAY, JCB, bank transfer, carrier billing, Paidy — through a single integration. |

| Access to Japan’s payment network | Japan’s payment networks each have their own compliance requirements and merchant agreements, conducted in Japanese, and require you to have a local registered entity or intermediary to offer their payment methods. | KOMOJU is a registered payment service provider in Japan. When you integrate, you inherit those agreements. No local entity required, no separate negotiations. |

Sources

Japan METI — FY2024 eCommerce Market Survey (published August 2025) · METI — 2024 Cashless Payment Ratio · PayPay Corporation — 70 million users, July 2025 · Rakuten Group — international merchant expansion, September 2025 · PCMI E-commerce Data Library · US International Trade Administration Japan eCommerce Country Commercial Guide · JACCS Payment Solutions consumer survey 2022 · KOMOJU internal research.